Seven Manufacturing Insights and What They Mean for You

The Industrial economy continues its strong rebound. Manufacturing data is strong though off post-pandemic peaks. Concerns center around scarce labor with rising wages, scarcity of semiconductors and higher input prices.

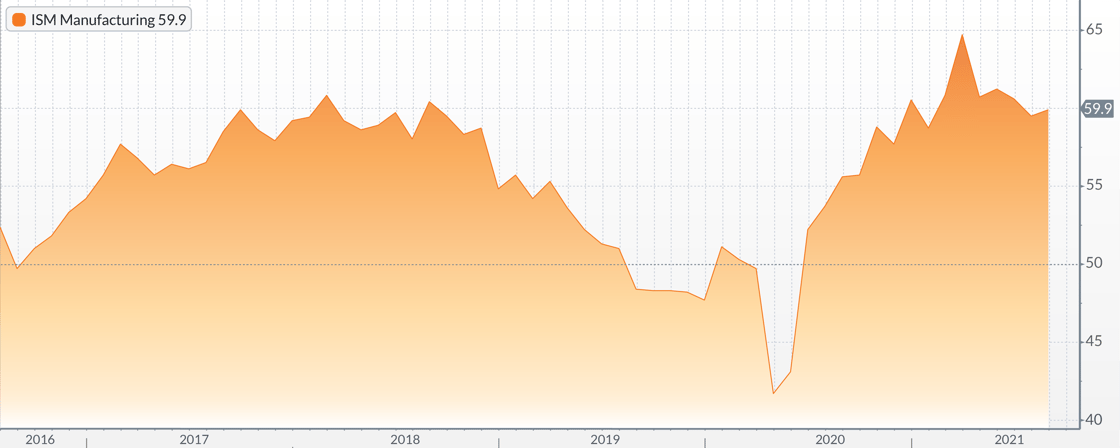

1. ISM Manufacturing – down from peak, but signaling expansion

With expansion above a score of 50, ISM Manufacturing is signaling strength across the manufacturing sector.

What this means for you: Continue to invest in the business for growth. However, make plans should the trends continue down toward the 50-55 range.

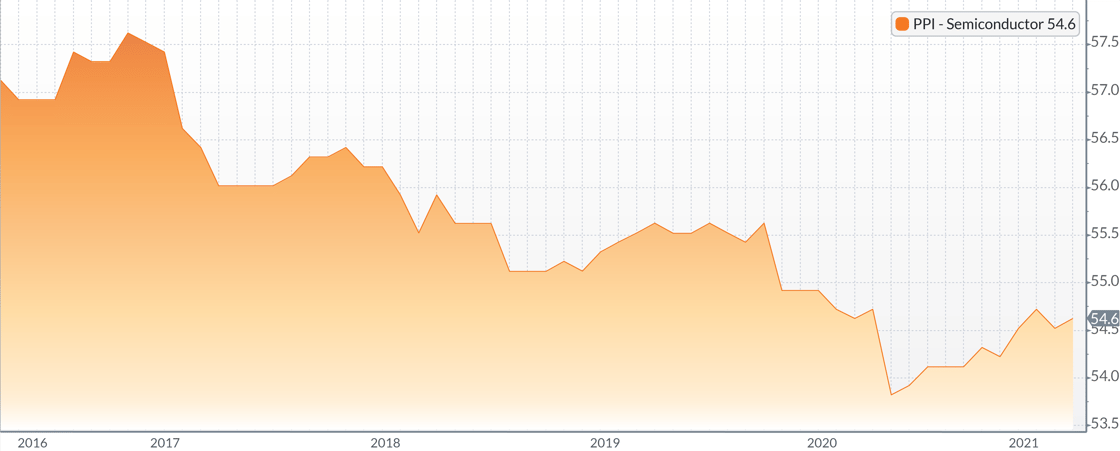

2. PPI Semiconductor – prices increase, reversing long-term trends

The shortage in semiconductor capacity has crippled many industries, such as automotive. These components have historically been deflationary, yet for the last year pricing has trended up due to capacity shortages.

What this means for you: Consider additional sources of supply as well as pricing strategies that assume shortages will continue well into 2022 and 2023 when larger manufacturers such as Taiwan Semi and Intel are able to add capacity.

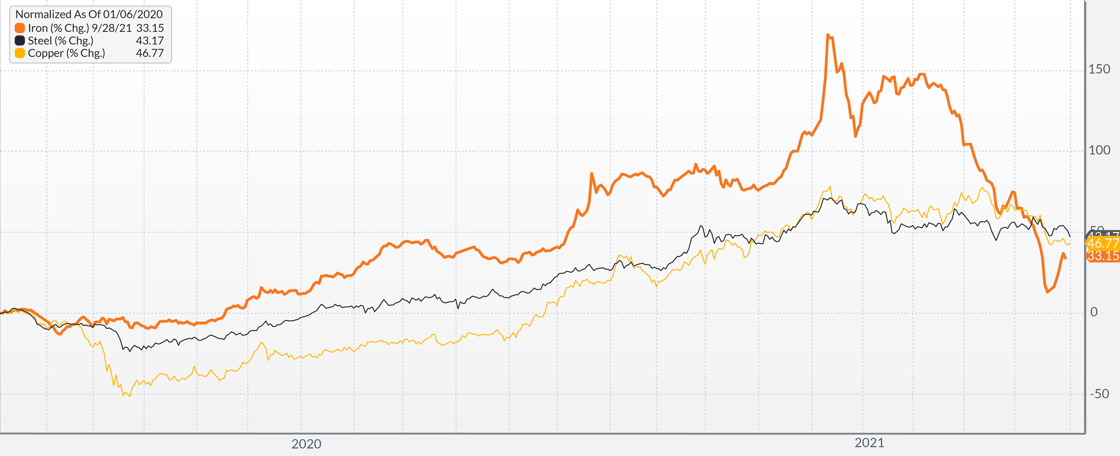

3. Commodities trends in iron ore, steel & copper falling

Constrained supply chains and increasing demand have resulted in prices 45-55% higher than the start of 2020. Yet iron, which had peaked at 155% higher than January 2020’s price, crashed this summer as China reduced steel production thus it’s need to import iron ore.

What this means for you: Manage procurement and pricing with an assumption that commodity prices will remain elevated, and could rise into 2022. Until Covid-related impacts on supply chains and staffing return to normal levels, commodity prices have the potential to remain higher than normal.

Adam Beckerman is the partner-in-charge of Aprio’s Manufacturing and Distribution group, one of the largest Aprio practices. Adam leads a team of 30 Aprio professionals who focus on the manufacturing industry. He has a 20+ years track record of enabling the success of manufacturing start ups, growth companies and businesses preparing for equity events. Schedule a consultation.

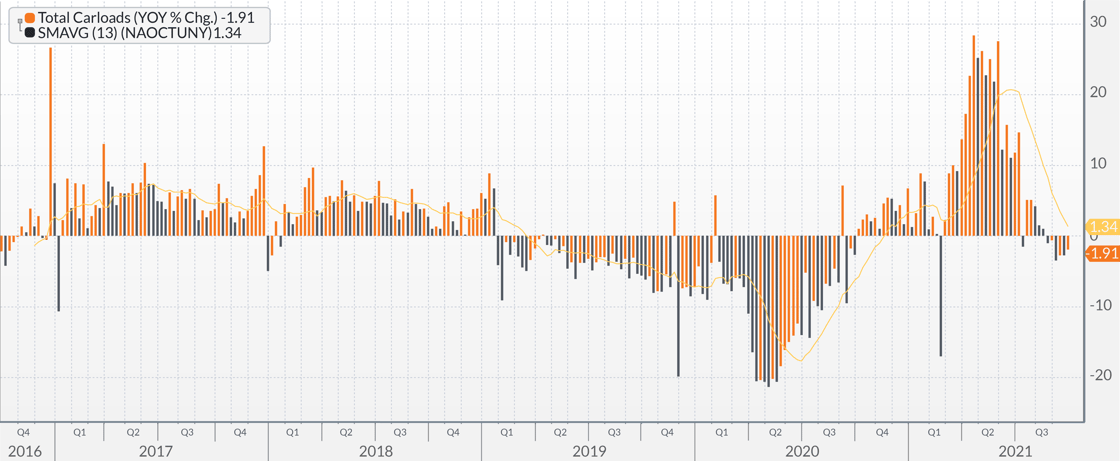

4. Total railcar loads are declining

Year-over-year railcar volumes have fallen recently, driven by significant declines in motor vehicles, equipment, intermodal containers, trailers, and agricultural and food products, that have been impacted by semiconductor capacity shortages, and port congestion.

What this means for you: Railroads may face difficulty delivering loads on time. Railroad carriers may adjust route networks and schedules to reflect lower volumes driven by the very well-known supply chain challenges.

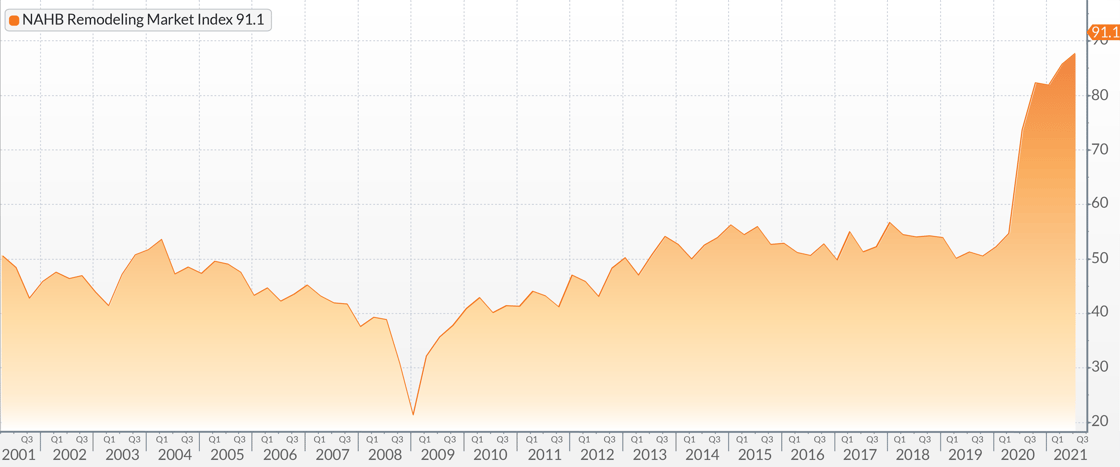

5. NAHB Remodeling Index current condition creates record levels

The Covid-related spike in spending on housing continues. With consumer balance sheets healthy, a low cost of financing and a growing economy, companies tied to home remodeling are expressing significant optimism about current conditions. The high end of the remodeling market (projects $50,000 or more) saw the largest increase in optimism.

What this means for you: Demand should be strong for remodeling work and those who supply products for remodeling. The greatest challenges are likely to be labor and input prices for manufacturers. Expect that strong environment to continue.

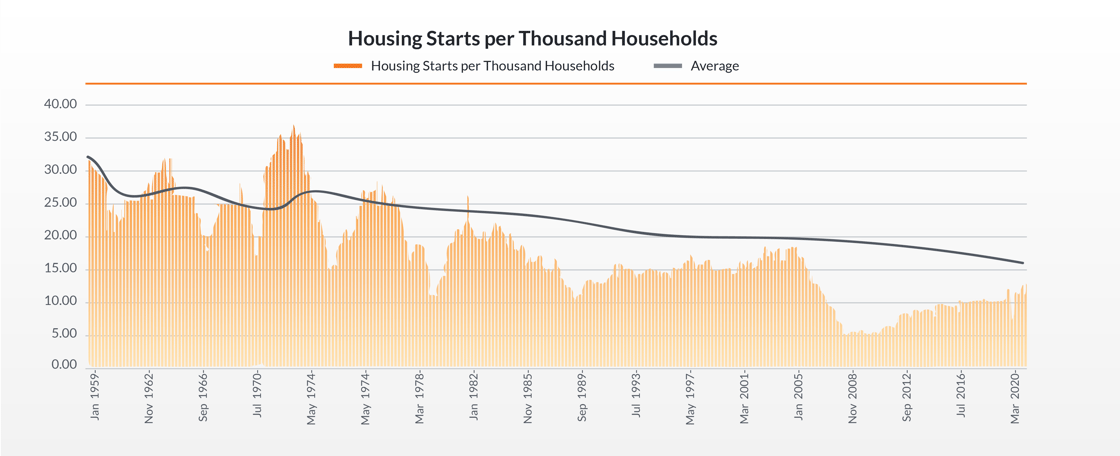

6. Housing starts need to increase 37% to return to average

Compared to historical needs for home starts per capita, the US is currently under-producing homes relative to its population. We believe the market is about 25-35% below a normal level.

What this means for you: Manufacturers, and other industries tied to residential housing, are likely to have several years of positive demand ahead. At the same time, competition for labor and higher input costs are likely to move along with demand, so optimizing those expenses will be critical to maximizing profitability.

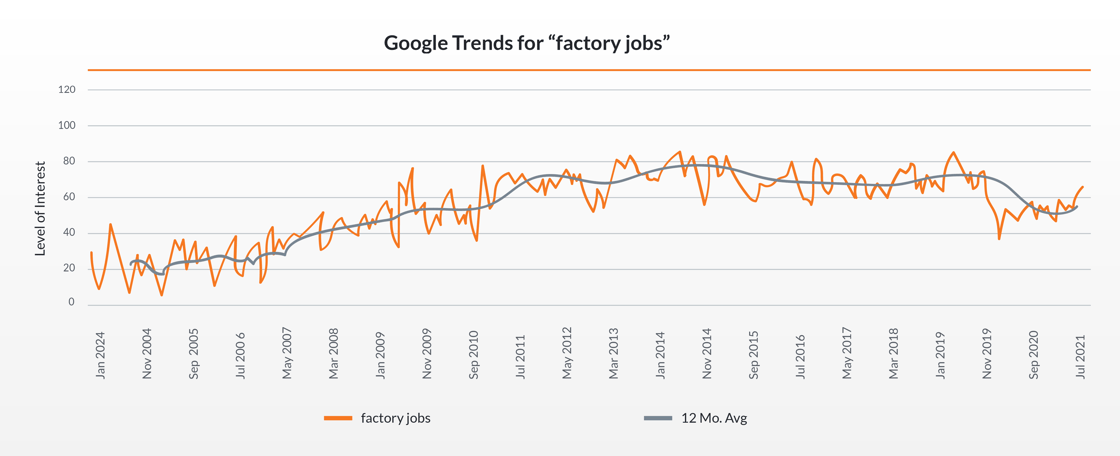

7. Google searches indicate increasing interest in factory jobs

After plateauing, the searches for factory jobs have picked up. This reflects an increasingly tight job market, rising wages and demand from manufacturers.

What this means for you: If recruiting factory labor, assume there is more interest and that there will be competition for that labor, so wage pressures may ensue. Consider using referral bonuses and other means to compete for talent.

Simeon Wallis is the Chief Investment Officer at Aprio Wealth Management, and the Director of Aprio Family Office. Each week Simeon brings you insights from the financial markets in Aprio’s Pulse on the Economy. To discuss these ideas and how they may affect your current investment strategy schedule a consultation.

Disclosure

Investment advisory services are offered by Aprio Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisor. Opinions expressed are as of the current date (October 12th, 2021) and subject to change without notice. Aprio Wealth Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Aprio Wealth Management, LLC’s investment advisory services.

Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Any securities mentioned in this commentary are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful.

Securities offered through Purshe Kaplan Sterling Investments. Member FINRA/SIPC. Investment Advisory Services offered through Aprio Wealth Management, LLC, a registered investment advisor. Aprio Wealth Management, LLC and the Aprio Group of Companies are not affiliated with Purshe Kaplan Sterling Investments.

Aprio, LLP, 5 Concourse Parkway, Suite 1000, Atlanta, Georgia 30328

%20(1)-Oct-06-2021-05-41-48-80-PM.png?upscale=true&width=1120&upscale=true&name=General%20images%20for%20resizing%20purposes%20(Amit%20Michaeli)%20(1)-Oct-06-2021-05-41-48-80-PM.png)